According to BNZ Bank news, BNZ Bank is taking action to limit the amount of debt that new borrowers can assume, and to implement a debt-to-income ratio for some of its loans.

The debt-to-income ratio (DTI) limits the amount someone can borrow relative to the income they earn-BNZ’s DTI will be set at 6, but it will be “constantly monitored and reviewed”. A DTI of 6 means that someone who borrows 600,000 NZD needs to have 100,000 NZD income. It is similar to the loan-to-value ratio that banks must currently apply. It limits the amount a person can borrow relative to the size of his deposit. BNZ is changing the way it assesses loans and customers’ overall debt levels to ensure that they are in a safer position when interest rates rise. source: BNZ tightens borrowing restrictions for low income borrowers [28 Oct 2021] https://www.nzherald.co.nz/nz/politics/bnz-tightens-borrowing-restrictions-for-low-income-borrowers/G4PWFHV7NU6COP7TWJDVSRRFRQ/

5 Comments

ASB is offering a 1.79% floating rate mortgage on loans used to buy newly built houses.

On 10 May, ANZ, one of New Zealand's biggest banks, has announced they would decrease the percentage of rental income they take into consideration when assessing new home loan application from 75 per cent to 65 per cent effective from 13 May.

According to Prime Minister Jacinda Ardern and Finance Minister Grant Robertson announce on 23 MARCH 2021..

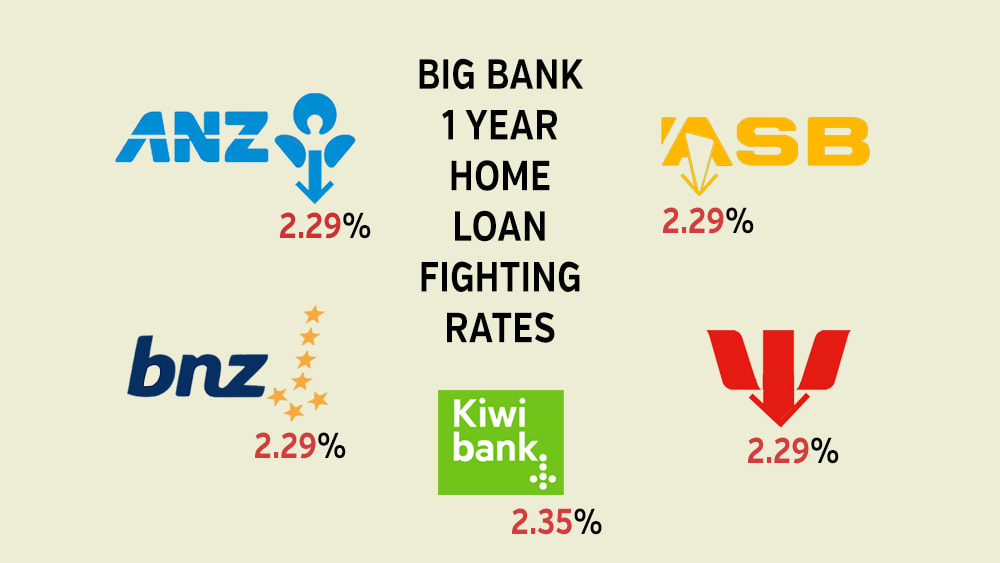

More banks are falling into line with carded rate cuts to home loans. BNZ is the latest. They have adopted the 2.29% one year fixed rate first claimed by Westpac. But they have also trimmed their two year rate to 2.59% and matching ASB for that term. It is starting to look like trailing banks are going to do the minimum to remain competitive. ASB has also now cut its one year fixed rate, also to 2.29%. Kiwibank have announced their one year fixed rate will reduce to 2.35% on Monday, January 25, 2021. Carded rate changes are one thing, but on the front lines, most banks will match the market lows of their main rivals if you ask them (provided your financials are attractive enough). Currently, the lowest one year rate is from Heartland Bank at 1.99%. The lowest 18 month rate is from HSBC at 2.25%. The lowest 2 year rate is from Heartland Bank and HSBC at 2.35% and TSB's 2.49% also undercuts the main bank levels. If banks use that funding line, they can still keep their margins intact with rates down to about 2%. Remember, the RBNZ's Funding for Lending program is in place, allowing banks to access money at the OCR's 0.25%. Only one bank has drawn $1 bln in the FLP line late so far, doing so late last year. $1 bln is enough to fund about 2000 home loans. In today's move, BNZ did not change any of its term deposit offers at the same time. Chaston, D. (2021, January 22). BNZ CUTS MORTGAGE RATES NOW TOO, QUICKLY FOLLOWED BY ASB. Interest.Co.Nz. https://www.interest.co.nz/personal-finance/108714/more-big-banks-slip-line-lower-one-year-fixed-rate-home-loan-offers-bnz  The number of houses sold nationally in December was up +42% from the same month in 2019, reaching 8935 in the month. But the REINZ claims there was a "lack of choice" in real estate markets nationwide at the end of 2020, resulting in sharply rising prices. Nationally, prices were up +19.3% compared to the same month a year ago, but the median price was up +$4000 to $749,000 from November to December, only a +0.5% rise. (REINZ revised down their November median price from the $749,000 they reported last month.) In Auckland, 3219 houses were sold in December, up from just 1932 in the 2019 equivalent month. Additionally, Auckland’s median house price increased by +17.4% from $886,000 at the same time last year to $1,040,000 a new record high, and the fifth consecutive month where Auckland has seen a new record median house price. Auckland central city area remains New Zealand’s most expensive district in the country with December seeing these suburbs reach a new record median house price of $1,280,000 – hovering extremely close to the $1.3 million mark. Not far behind, was North Shore on $1,235,000 and Rodney district on $1,005,000 showing how unaffordable the Auckland region is becoming – especially for first home buyers. The only district in Auckland now with a median under the $800,000 mark is Franklin district with a median of $790,000. New Zealand house prices rose at an average of $332 per day in 2020. They rose at a slower rate in December, gaining a more modest $129 per day during December at the median level. In Auckland, the December gains were +$323 per day, taking the annual daily gain rate to +$422. On a proportional basis, gains were high in many other regional centers too. In total 11 regions saw record median prices during December 2020. In December, the median number of days to sell a property nationally decreased 4 days from 31 to 27 when compared to December 2019, the lowest in 204 months (since December 2003). Across the country, 14 out of 16 regions had a median number of days to sell of less than 30 days which is the highest on record. Only Northland and the West Coast were exceptions. For New Zealand excluding Auckland, the median days to sell decreased by 4 days from 30 to 26. Auckland saw the median number of days to sell a property decrease by 5 days from 34 to 29, the lowest for the month of December in 17 years. Taranaki had the lowest days to sell of all regions at 20 days – down 7 days from the same time last year. This was the lowest days to sell for Taranaki since records began. Additionally, Waikato (24), Bay of Plenty (27) and Manawatu/Wanganui (21) had record low median days to sell. Chaston, D. (2021a, January 15). Demand exceeds supply in housing markets - result is higher prices. Interest.Co.Nz. https://www.interest.co.nz/property/108601/2020-capped-19-rise-house-prices-year-despite-sharp-jump-volumes-sold-prices-were Westpac has launched into 2021 with a sharp cut in a key mortgage rate. They have cut -20 bps from their one year 'special', taking it down to 2.29%. This is the first cut in a fixed rate from any bank since November 6, 2020, nine weeks ago. But it won't be the last. The RBNZ's Funding for Lending program is in place, allowing banks to access money at the OCR's 0.25%. If banks use that funding line, they can still keep their margins intact with rates down to about 2%. One bank has drawn $1 bln in the FLP line late last year. $1 bln is enough to fund about 2000 home loans. Westpac is aiming to capitalise on the housing frenzy underway. “We know property ownership has probably been a hot topic for many Kiwi families over the holiday period, so whether you’re looking to buy your dream home in 2021 or just pay off your mortgage a bit faster, this special rate could help you get there,” a spokesperson says. “Two years ago the same special home loan rate over the same term was 4.15%. It would have cost $1,119 a fortnight to service a $500,000 mortgage over 30 years. Now, the lower interest rate means the same repayment would be $885 a fortnight – a saving of $6084 over a year.” Their new offer is effective today, Monday, January 11, 2021. Westpac's eligibility criteria included a minimum of 20% equity, plus salary credit to a Westpac transaction account, to be issued prior to drawdown date. These special fixed interest rates cannot be used in conjunction with any other Westpac home loan offers or discount packages, including previously negotiated offers, legal fee contributions or the Westpac Choices Home Loan with Airpoints™. These special fixed interest rates do not apply to loans for business or investment purposes. Westpac is also reducing its Bonus Saver by -5 bps to 0.20% pa and the interest on its Notice Saver by -10 bps to 0.40% pa. Given the FLP, it is hard for banks to justify any offer over 0.25% pa. Despite today's sharp cut by Westpac of their home loan rate (the lowest one year rate by any major), it is not the lowest one year fixed rate available. HSPC offers the same term at 2.25%, and Heartland Bank still has a 1.99% fixed offer for one year. Chaston, D. (2021, January 11). WESTPAC LAUNCHES A 2.29% ONE YEAR FIXED HOME LOAN RATE. Interest.Co.Nz. https://www.interest.co.nz/personal-finance/108562/encouraged-rbnz-one-major-bank-offers-229-one-year-fixed-home-loan-rate-it  House-price inflation is New Zealand’s hot-fire issue. Look back a year and very few people were predicting the fire. Now we have a fireball.

Quite simply, house-price inflation is driven by citizens’ loss of confidence in fiat currency. Having money in the bank has become a mug’s game. As long as post-tax interest rates on savings are well below inflation rates, then the fireball cannot be doused. Investors have to find somewhere for their savings. Prior to COVID19, there was a valid argument that urban planning rules combined with high immigration were the key drivers of house-price inflation. Those urban-planning issues had been in the background for many years but were then fanned by high immigration. However, it is COVID-19 and the reactions of the State, particularly monetary policy under the control of the Reserve Bank, that have created the current fireball. The current Reserve Bank inflation mandate belongs to another time The Reserve Bank Governor has made it explicit that house-price inflation is not a central issue to the Reserve Bank mandate. In a technical sense, that is correct. However, house-price inflation is central to the future of New Zealand, and any sense that we can be a property-owning team of five million. As long as monetary policy was focused on flattening short-term business and spending cycles, then independence of the Reserve Bank using standard monetary tools made a lot of sense. Some things are indeed best left out of the hands of politicians. However, monetary policy has strayed into areas well outside historical norms. Interest rates have been declining globally for much of the last 20 years. That aligns with global growth rates declining everywhere. China is the outlier, but even there, economic growth as a percentage of the economy has been declining, and so have interest rates. Since COVID-19, the extraordinary measures of quantitative easing have been extraordinarily successful in artificially reducing interest rates even further, particularly across the Western World. And there lies the issue. Back in June I wrote about the flood of capital entering the market via the Reserve Bank’s quantitative easing programme. I tried to forewarn of the risks from excessive quantitative easing. However, at that time, most people were focused on more immediate issues relating to COVID-19 and jobs. Right through to the election, the issue of house prices remained in the background. It is now no longer possible to obtain a bank interest rate that protects against inflation, yet the Reserve Bank is trying to increase inflation further. To at least some of us, it is a crazy world. The increasing growth of digital block-chain currencies is another sure sign of a global loss of confidence in fiat (national) currencies. These digital currencies, led by bitcoin but with others in the wings, are highly speculative and have no inherent value. However, with confidence in fiat currencies declining, the search for alternative nest eggs expands. Hence, people are drawn to these digital currencies. Once again, it is the consequence of a crazy world. The rush to investment properties Here in New Zealand, the rush by investors to purchase investment properties is not driven by any fundamental wish to be landlords. Rather, it is driven by a belief that there is nowhere else to go. Accordingly, under current place settings, there is still a long way for house price inflation to run. There are still many billions of dollars – indeed approximately $200 billion - sitting in current accounts and term deposits with the citizen owners of those funds now becoming very scared. Unfortunately, the Reserve Bank has very limited expertise when it comes to behavioural sciences. Their only tools for assessing behavioural changes that lie outside historical norms are to operate through a rear vision mirror. Accordingly, they have been and continue to be badly caught out as to what they have created. Their response is that the housing crisis is a ‘first class problem’, largely outside their mandate. If ‘first class’ problem means a huge problem, then it is hard to disagree with that assessment. But if it means something else, and the evidence is clear that Reserve Bank Governor Adrian Orr does indeed mean it in a different context, then once again it is evidence of a crazy world unsuited for a team of five million. House inflation does not soak up excess money supply Very few people recognise that house-price inflation does not soak up the excess money that the Reserve Bank is creating. Every time someone buys a house there also has to be a seller. Money simply flows from one bank account to another. The same principle applies with shares. It helps explain why bubbles keep growing until they pop. This fundamental fact as set out above is why there is a fair chance that we are still in the early stages of the house-price inflation firestorm. The only qualifier on that statement is if there is a change of Reserve Bank policy in regard to quantitative easing and hence interest rates. In the meantime, there is nothing to stop house price inflation from continuing as savers flee the banks. Band-aids focus on the wounds rather than the cause Some may think that the firestorm can be controlled by other means such as rent freezes and extending the bright-line taxation test for investor housing. But they are mistaken. Such measures focus on outcomes rather than cause. Rent freezes are extremely bureaucratic and can lead to multiple unintended consequence. It takes one back to the Muldoon days of wage and price freezes. These measures can douse a few flames but the flames soon return. This is because the fundamental issues lie elsewhere. Increasing the bright-line period for capital gain taxation may also slow things down a little, but as long as savers have nowhere else to put their money, then the effects will be limited. If bright-line is to be extended then it needs to exclude newbuilds. Quite clearly, there is a need for newbuilds to continue. Increasing loan to value requirements will surely have some effect. However, the likelihood is that it will affect first home buyers more than investors. The Reserve Bank could limit new restrictions to investors, but that would imply that the Reserve Bank was acting in a social context rather than a financial stability context. And that is on not how the Reserve Bank Governor thinks. The Reserve Bank Governor has now asked for debt-to-income tools to be made available to him. That tool, if granted, is likely to constrain first-home owners much more than investors. There are no painless solutions to self-created problems If the Reserve Bank really wants to control the so-called ‘first class problem’, then it has to rein back severely on its quantitative easing (QE) programmes. Reining back on QE means less digital money creation and thereby leaving more Treasury bonds out in the market place. At that point interest rates will stabilise and in high likelihood start to drift upwards again. Some savers may then begin to think that their bank deposits have some safety. Of course, higher interest rates will be very unpopular for those who now have big mortgages. That illustrates that there are no painless solutions. Accordingly, our politicians have good reason to be cautious of declining house prices. However, the immediate aim is not to drop house prices. It is simply to put out the current inflationary fire. Quite simply, the longer the fireball continues, the greater the long-term pain must be. And the more that any notion of a team of five million can only be an irony. Interest rates cannot be changed in isolation If the Reserve Bank steps back from QE but does nothing else then there may well be some damaging effects. In particular, there will be an inward flow of speculative funds from overseas and the exchange rate will rise. That will have to be addressed. This illustrates how over the last thirty years New Zealand has become closely integrated within the American and European international financial system. Arguably, that has worked well, and has helped create financial responsibility here in New Zealand. But these are now very different times. It is a strange world where our physical economy aligns primarily with the East but our financial systems align with the West. One ready tool the Reserve Bank does have to sit alongside the reining in of the QE system is to require New Zealand banks to place increasing reliance on NZ-resident funds. That is simple; it is just the stroke of a regulatory pen. Nothing will change without a change in the Reserve Bank inflation mandate The current actions of the Reserve Bank all stem from the specific mandate that requires them to keep consumer price inflation between one percent and three percent, and with a long-term aim of two percent. This target is a consequence of a deep-seated belief within mainstream economics that inflation of this level is necessary to somehow stimulate productive investment. An alternative perspective is that these mainstream economists have got confused between cause and effect. Even then, the relationship belongs to another time. I have previously argued that reducing the inflation target by one percent, so as to lie within a range of zero to two percent would have a transformational effect. That is where the target used to sit twenty years ago. It would immediately mean that the New Zealand consumer inflation rate was within target and therefore QE could be reined in. To the extent that economic stimulus is still required, it would also place the emphasis firmly back on fiscal policy. But most importantly, it would be the first step to prevent saving behaviours being a mug’s game. And that would take a lot of heat out of the housing market. A New Year’s wish directed at Grant Robertson I hope that Grant Robertson will spend the summer break reflecting deeply on the long-term impact of the current Reserve Bank mandate. The consequence of that mandate is that pathways for young people without parental financial support to become part of a property-owning team of five million have largely disappeared. Accordingly, major social inequalities are being further institutionalised. For a Labour Government, this must be a real irony. Grant Robertson is the only person who can change that. Woodford, K. (2021, December 26). House-price inflation and interest rates are bound at the hip. Interest.Co.Nz. https://www.interest.co.nz/opinion/108516/reducing-house-price-inflation-depends-identifying-drivers-right-now-means-interest  They aren't called holiday hot spots for nothing, with real estate prices rising at a scorching rate in many of the country's favourite holiday destinations.

Sales figures from the Real Estate Institute of New Zealand show median selling prices in many popular holiday destinations had percentage increases well into double digits over the three months to the end of November compared to the same period of last year. The biggest increase of 58% was in the village of Akaroa on Banks Peninsula, although the increase for the whole of the peninsula was only 6%. Other areas with very high annual price increases were Waihi Beach, up 50%, and Hokitika which was up 41%. Perhaps surprisingly, the three locations that recorded annual decreases in their median prices were Coromandel Town -11%, Onetangi on Waiheke Island -17% and Te Anau -3% (see table below for all districts). REINZ chief executive Bindi Norwell said the drop in median prices at Onetangi could have been due to a downturn in Airbnb bookings, which could have prompted more owners to sell. However the volume of properties sold at most of the holidays destinations was higher than it was over the same period of last year. Ninness, G. (2021, December 17). Surge in property prices and sales volumes in holiday hot spots. Interest.Co.Nz. https://www.interest.co.nz/property/108452/property-prices-have-surged-akaroa-and-waihi-beach-there-were-surprising-price-falls The country's largest home lender ANZ says from now it will require investors to have 40% deposits.

This goes further than the recommendations of the Reserve Bank, which is moving to have 30% deposits for investors in place by March. It comes as the housing market has absolutely taken off with prices having risen by 18.5% in the past 12 months. The RBNZ is currently consulting to reintroduce loan to value ratio (LVR) restrictions, which it removed in May. The proposal from the RBNZ is to reinstall the restrictions exactly as they were when removed in May. This means 30% deposits for investors and 20% for owner-occupiers, with banks able to lend up to 20% of their new mortgage lending for loans in excess of 80% of the value of the property (IE for deposits of under 20%). Most major banks have already adopted these rules ahead of the planned March reintroduction. But now ANZ has gone further. The 40% deposit level for investors actually aligns to what the requirement was back in mid-2016 when, with more than a hint of desperation, the RBNZ slammed 40% deposits on all investors. It worked. Subsequently these rules were relaxed over the past two years as the heat came out of the housing market. In the New Zealand market, ANZ is a very big player. It accounts for just under a third of the total mortgage lending. ANZ Managing Director Personal Ben Kelleher said the bank's decision followed two months of record levels of mortgage lending. In those two months some 32.4% of the new mortgage lending had gone to investors, while 18.3% had gone to first home lenders. “Escalating property prices are putting home ownership out of reach for many Kiwis," Kelleher said. "The current settings favour property investors particularly over first home buyers, potentially locking a generation of New Zealanders out of home ownership. “It’s in everyone’s interests for residential property prices to be sustainable long term, and for home ownership to be accessible to as many people as possible. “As New Zealand’s largest home lender, decreasing the LVR on residential investor lending is one thing we can do to help bring balance to the residential property market.”. Here is the announcement from the ANZ: ANZ Bank NZ today announced it would require a 40% deposit from residential property investors as a step to bring balance to the housing market. Effective immediately, investors will need equity of 40%, up from the current 30%, when borrowing to buy residential property. There are no changes to deposit requirements for other residential buyers, including first home owners. ANZ Managing Director Personal Ben Kelleher said ANZ would also be recommending to the Reserve Bank of New Zealand (RBNZ) as part of the current consultation that loan-to-valuation ratios (LVR) be set at 60% for residential property investors, rather than the 70% that has been proposed. “We’ve been closely monitoring the impact on residential property prices of historically low interest rates, reduced LVR requirements and existing issues with supply and demand,” Mr Kelleher said. “Escalating property prices are putting home ownership out of reach for many Kiwis. The current settings favour property investors particularly over first home buyers, potentially locking a generation of New Zealanders out of home ownership. “It’s in everyone’s interests for residential property prices to be sustainable long term, and for home ownership to be accessible to as many people as possible. “As New Zealand’s largest home lender, decreasing the LVR on residential investor lending is one thing we can do to help bring balance to the residential property market.” ANZ has seen two record months of residential property lending with 32.4% going to residential property investors and 18.3% to first home buyers. He said ANZ would longer term be guided by the outcomes of the RBNZ’s consultation process early next year. Hargreaves, D. (2020, December 15). The country’s largest home lender has announced a more strict lending. Interest.Co.Nz. https://www.interest.co.nz/opinion/108413/countrys-largest-home-lender-has-announced-more-strict-lending-policy-housing  Wearing a mask on public transport in Auckland and flights all around the country will become mandatory from Thursday morning. Cabinet on Monday agreed the rule will apply to passengers over 12 years of age on buses and trains within Auckland, as well as those travelling in to and out of Auckland. The rule will apply to all domestic flights. Taxi and Uber drivers will need to wear masks, but their passengers will be exempt. The rule comes into force at 11.59pm on Wednesday. Police, but not bus drivers, will be able to enforce it. Here’s a press release from the Government: Masks will need to be worn on all public transport in Auckland and in and out of Auckland and on domestic flights throughout the country from this Thursday, Minister for COVID-19 Response Chris Hipkins said today. “I will be issuing an Order under the COVID-19 Response Act requiring the wearing of face coverings on all public transport into, out of and through the Auckland region, including for taxi and Uber drivers, and on all New Zealand passenger flights. This will come into force at 11.59pm on Wednesday 18 November,” Chris Hipkins said. “Adding mask wearing to the toolbox of measures against the virus is a sensible precaution and the time is right to make the move. “As we learn more about the virus and continue to strengthen our test, trace and isolate processes and border measures, modelling is now telling us that we’re at the stage of having the toolset that means we’re better able to respond to community cases with fewer restrictions. “That’s not to say that won’t happen. But we’re in a much better position to avoid blunt and costly lockdowns by being able to control the spread of the virus with a flexible mix of measures that best fit the situation. “In this light, and taking all factors into account, we’ve determined that now is the right time to make mask use mandatory in these situations. It will provide another line of defence, is a low-cost and practical option and presents a minor inconvenience by comparison. “When we use and dispose of face coverings correctly, they can both reduce the risk of infected people infecting others, and help protect uninfected people from catching the virus. “It’s also a good visual reminder that while New Zealand remains relatively free of restrictions, we’re not out of the woods yet. We’re at Level 1, not Level zero. From 11.59pm on Wednesday 18 November, the use of face coverings will be mandatory for: · people travelling on public transport services in into, out of the Auckland region (except for children – under 12 years of age); · people travelling on passenger flights throughout New Zealand.· the drivers of small passenger service vehicles in Auckland, such as taxis and app-based ride services, but not their passengers; and, Children and young people travelling to and from school are exempt from face covering requirements on school buses and other school transport. A full list of exemptions will be on the COVID-19 Government website. “We will take an ‘educate and encourage’ approach. Police can enforce the new rules – but this will be a last resort. Bus drivers and other transport workers will not be responsible for enforcing the new requirement.” The new move is in line with the measures already taken and fits with New Zealand’s overall focus on keeping the virus out and stamping it out when cases appear, Chris Hipkins said. “Decisions to introduce mandatory measures are not taken lightly. They are based on expert advice from a range of scientific and public health disciplines and seek to strike the right balance between maximum efficacy and practicality. “Combatting COVID-19 requires a sustained effort from all New Zealanders and there are simple actions everyone can take to keep us safe. “It’s important we all still follow good hygiene such as handwashing, cough and sneeze etiquette and staying home when sick. Scanning QR codes continues to be a key tool for contact tracing,” Chris Hipkins said. “The Government is seeking further advice from officials about extending face covering requirements for other centres and introducing mandatory scanning of QR codes in some high risk situations where contact tracing is challenging.” “As Covid-19 Response Minister, I am also working with colleagues on a wide range of other significant work streams that will help keep us ahead of the curve and safe, while supporting our economy. “These include enhanced testing and contact tracing for border workers, MIF booking and allocations, a review of PPE use for MIF workers, airport arrangements, safe travel zones and a greater use of technology,” Chris Hipkins said. Tibshraeny, J. (2020b, November 16). Mask-wearing to become mandatory on public transport in Auckland and flights around the country from Thursday. https://www.interest.co.nz/news/107985/mask-wearing-become-mandatory-public-transport-auckland-and-flights-around-country  Cabinet has agreed to make the Small Business Cashflow Loan Scheme accessible for a longer period of time. Businesses will now have until December 31, 2023 to apply for unsecured loans under the scheme, administered by the Inland Revenue Department. The deadline was previously December 31, 2020. The interest-free period of loans under the scheme will also be extended from one year to two years. And the criteria for what the loans can be used for will be broadened beyond core business operating costs to capital items. Labour campaigned on these changes ahead of the election. Under the Small Business Cashflow Loan Scheme, “viable” businesses can get a $10,000 loan. The size of the loan can be extended by $1800 for every full-time equivalent employee the business has up to 50 employees. So, the maximum available is $100,000. Finance Minister Grant Robertson said that before the end of the year, Cabinet would consider allowing businesses that have repaid their loans to take out another loan under the scheme, increasing the cap to make larger loans available and/or adjusting the eligibility criteria. Robertson said legislation would be required for some of these changes. Loans are subject to 3% interest when the interest-free period expires. This interest is charged from the date the loan is drawn down. Loans need to be repaid within five years of them being taken out. Close to 100,000 businesses have received a loan under the scheme to date, with lending totalling $1.6 billion. The average value of each loan is $17,000. Tibshraeny, J. (2020). BUSINESSES ABLE TO ACCESS INTEREST-FREE GOVT LOANS FOR ANOTHER 3 YEARS. Interest.Co.Nz. https://www.interest.co.nz/business/107873/cabinet-agrees-extend-small-business-cashflow-loan-scheme-three-years-will-consider  The Government is offering to underwrite larger bank loans to businesses via its under-subscribed ‘Business Finance Guarantee Scheme’ (BFGS). It’s increasing the cap on loans offered under the scheme 10-fold, from $500,000 to $5 million. It’s also broadening the BFGS to enable businesses to use the loans for purposes beyond cashflow. They can now use the loans for "capital assets and projects related to responding to, or recovering from, the impacts of Covid-19". They can also re-finance up to 20% of their existing debt. Larger businesses, with annual revenue of up to $200 million, are also eligible. This cap previously sat at $80 million. And the Government is increasing the maximum term of loans from three years to five years. If a business defaults on a loan under the BFGS, their bank will follow its normal process to recover the debt. If the debt can’t be recovered, the bank can claim 80% of any shortfall from the Crown. By shifting the bulk of risk from the bank to the Crown, the purpose of the BFGS is to encourage the bank to lend more freely. It’s ultimately a bank’s decision whether they lend to a business or not. While the Government doesn't require the bank to take security, or for the borrower to provide a personal guarantee, the bank can still chose to do so. RBNZ changes term lending facility The Reserve Bank has been backing the BFGS by offering to lend banks money at the Official Cash Rate provided they on-lend these funds under the scheme. Because the Government is increasing loan terms under the scheme, the Reserve Bank is likewise increasing the maximum term of its Term Lending Facility to five years. Participating banks - ANZ, ASB, BNZ, Heartland Bank, Kiwibank, SBS Bank, TSB, Bank of China and Westpac - have only drawn down $27 million from this facility to date. $150m lent under $6.25b scheme Banks have only lent $150 million to 780 customers via the BFGS. When Finance Minister Grant Robertson launched the scheme in March, when share markets were crashing, he expected businesses to borrow up to $6.25 billion. The scheme faced issues, as it was announced on the fly before banks were ready to receive applications. The eligibility criteria was also narrow, so had to be broadened in May to include agricultural businesses and smaller businesses. Robertson also did away with a requirement for banks to take security in some instances. While Kiwibank Chief Customer Officer for Business, Quentin Quin, said "a whole lot" more customers would now qualify for the scheme, NZ Bankers' Association CEO Roger Beaumont said "uptake will ultimately be driven by demand from businesses". Reserve Bank Deputy Governor Geoff Bascand last month noted there had been a "material decline in businesses’ demand for credit" (across the board, beyond the Business Finance Guarantee Scheme) over the first half of 2020. "While demand for loans for working capital from small to medium businesses, corporates and sheep and beef farmers has increased, demand for credit for capital expenditure has fallen significantly," he said. He casted doubt on the prospect on an immediate uptick, saying: "Businesses’ investment intentions have also fallen sharply, with increased uncertainty around the strength of future demand. "Some apparent weakening of demand for credit may also reflect perceptions by businesses that credit would not be available or that terms have tightened." Bascand has repeatedly urged banks to lend, to avoid adding a credit crunch to the economic crisis caused by Covid-19. Small businesses most in need Coming back to the BFGS, Treasury in March advised Robertson small businesses, not covered by the scheme, needed support more urgently. “The pressures will generally emerge first in smaller firms, which have fewer pre-approved precautionary loan facilities. Larger corporates have more options and deeper banking relationships,” Treasury said. “The banks still have capacity to provide support to their clients, notably large corporates that represent a good credit risk.” Indeed, the uptake of the subsequently announced, Inland Revenue-run Small Business Cashflow Loan Scheme, which offers unsecured interest-free loans of up to $100,000 to small businesses, has been huge. The BFGS is available until December 31. Tibshraeny, J. (2020, August 20). Robertson increases cap on Business Finance Guarantee Scheme 10-fold, extends terms of loans and enables businesses to use loans for capital investment and re-financing. https://www.interest.co.nz/business/106648/robertson-increases-cap-business-finance-guarantee-scheme-10-fold-extends-terms  The Reserve Bank (RBNZ) has agreed to help banks extend the mortgage repayment deferrals they’ve been offering their customers since the end of March. RBNZ Governor Adrian Orr confirmed this on Wednesday, further to his deputy, Geoff Bascand, a couple of weeks ago saying he didn’t want to see an abrupt end to the offering. Orr hoped to finalise details with banks next week. He urged people not to flood banks with inquiries, as the details of what will be offered are still being ironed out. “As always, an extension is not permanent,” Orr said. It is ultimately a bank’s decision whether it enables a customer to defer the principle and interest repayments on their mortgage. What the RBNZ can do is treat the loan as performing, rather than impaired. Impaired loans require banks to hold more capital against them. Bascand on July 31 said there were $20.6 billion of residential mortgages that had principal and interest payments deferred, and a further $18.3 billion of mortgages that had moved to ‘interest only’ since the onset of Covid-19. This represented 14% of the banking sector’s mortgage book. Tibshraeny, J. (2020). RBNZ to help banks enable their customers to defer mortgage repayments beyond 6 months; Details expected next week. Retrieved 12 August 2020, from https://www.interest.co.nz/property/106499/rbnz-help-banks-enable-their-customers-defer-mortgage-repayments-beyond-6-months |

Watch this spaceFollow us to see the latest news. Archives

October 2021

Categories |

RSS Feed

RSS Feed